The Algorithmic Guardrails: Why “Experiment” is a Dirty Word

When I launched canigetadollar.com, I thought the biggest hurdle would be convincing people to participate. I was wrong. The real challenge was convincing the banking algorithms that I wasn’t a criminal. In the eyes of a payment processor’s AI, a sudden influx of $1.00 transactions is the ultimate “Red Flag.” It looks like Card Testing—a tactic used by hackers to verify stolen credit card numbers.

To a machine, a thousand people joining a social experiment looks identical to a botnet testing a leaked database. I quickly learned that in 2026, “innovation” is often indistinguishable from “risk” to a line of code.

Physical vs. Digital: The “Friction” Paradox

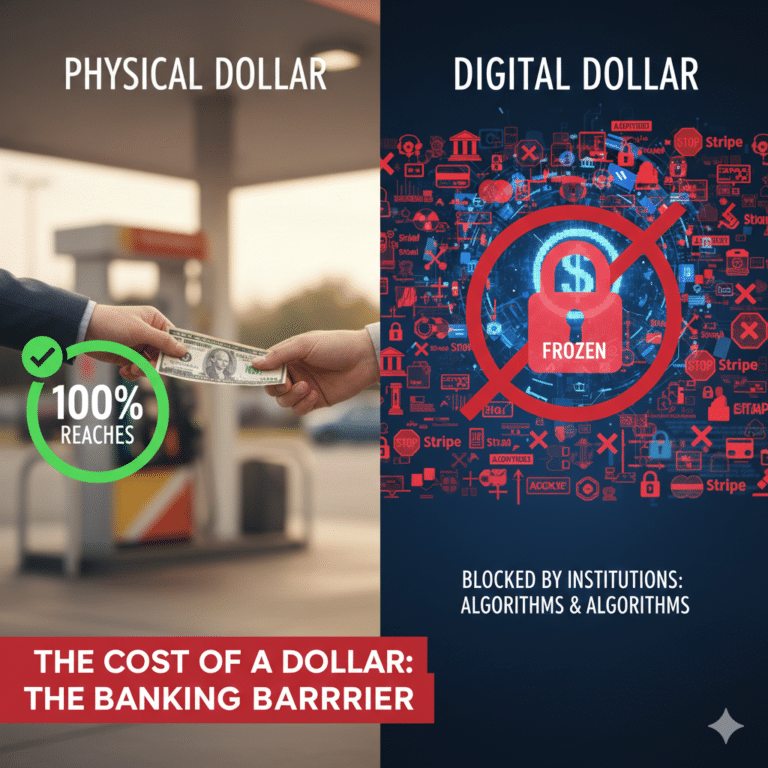

There is a profound irony in how society handles a single dollar. If you are standing at a gas station and someone asks, “Hey, can I get a dollar?” the transaction is frictionless. You reach into your pocket, hand over a bill, and the exchange is complete. No one asks for your ID, no bank takes a 30% cut, and the person receiving it has 100% of that dollar’s purchasing power instantly.

On the internet, that same request is a logistical nightmare:

- The Trust Gap: In person, you can look into someone’s eyes. Online, you are looking at a URL. To bridge that gap, we have to build elaborate “trust systems”—ledgers, “About” pages, and social proof—just to justify a transaction that would take three seconds on a street corner.

- The Invisibility of Cash: Physical cash is “silent.” The government and the banks don’t know it changed hands. But the digital dollar is “loud.” It leaves a trail of metadata, and because that trail is so thin ($1.00), it triggers every “spam” alarm in the financial system.

- The Burden of Verification: In the physical world, the “verification” is your own judgment. In the digital world, the verification is a series of CAPTCHAs, 3D-Secure prompts, and email confirmations. We’ve found that the “cost” of verifying a digital dollar is often higher than the dollar itself.

The “Donation” Deadlock: The Nonprofit Paradox

One of our biggest setbacks came when our primary processor suspended our account. Their reasoning? We were “soliciting donations without a 501(c)(3) status.”

This created a fascinating philosophical and legal deadlock. This project isn’t a charity; it’s a digital media study. However, because the “product” being sold is a spot on a public ledger—and the price is the symbolic $1.00—traditional banks don’t have a category for us. We exist in the gray space between “e-commerce” and “fundraising,” a space that the modern financial grid is designed to squeeze out.

The “Bank Tax”: When Fees Outpace the Fund

The most startling data point we’ve uncovered so far is the sheer cost of moving money. On a standard $1.00 transaction, the combination of flat fees and percentages can swallow up to 40% of the contribution. If the goal of this experiment is to see what “purchasing power” we can aggregate, we are fighting a war of attrition against the “Middleman Tax.” We’ve had to pivot through three different platforms—from Stripe to Buy Me A Coffee to Ko-fi—just to find a way to keep more than 60 cents of every dollar given. It turns out that being “generous” at a small scale is actually one of the most expensive ways to use the banking system.

Evolution through Friction: Turning Hurdles into Data

As frustrating as these freezes and bans have been, they have become the most valuable part of the experiment. We aren’t just documenting who gives a dollar; we are documenting the technological resistance to micro-scale collective action.

Every time an account is frozen, we learn something new about the “gatekeepers” of the digital economy. We are currently moving toward a more resilient “Ledger Entry” model to satisfy the banks, but the lesson remains: Scaling a simple “gas station ask” in a digital world requires a master’s degree in fintech survival.