In an era where you can order a pizza, buy a car, and trade stocks from your pocket, there is a lingering misconception that digital finance offers a cloak of invisibility. We often hear about “private” transactions or “anonymous” digital wallets, but the reality is far more transparent—and far more regulated.

If you are looking to move wealth without the government knowing exactly who you are, where you live, and how much you’re sending, the digital world is a dead end. Here is why true anonymity in electronic transfers has become functionally impossible, and why the “convenience” of the modern age may actually be a form of financial duress.

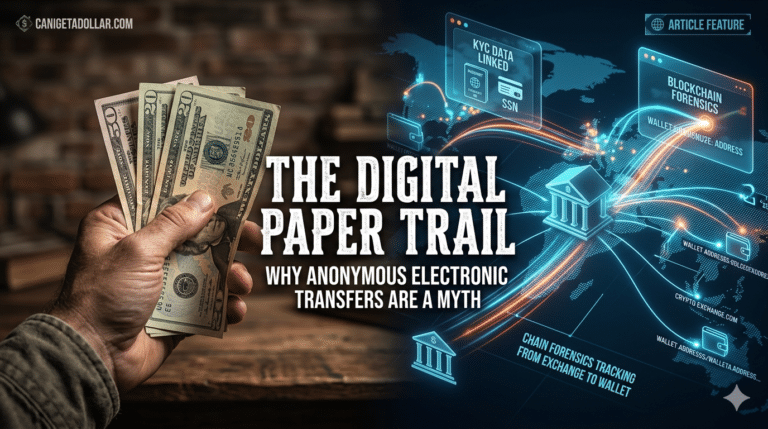

1. The Gateway: “Know Your Customer” (KYC)

The moment you try to interface with the modern financial system—whether it’s a traditional bank, a peer-to-peer app like Venmo, or a crypto exchange—you hit a brick wall called KYC.

Under federal law, financial institutions are required to verify the identity of their users. This isn’t just a simple name-and-email sign-up. To move any significant amount of money, you must provide:

- Your legal name and residential address.

- Your Social Security Number (SSN) or Taxpayer Identification Number.

- A government-issued photo ID.

This information isn’t just sitting in a private vault; it is the “digital tether” that connects your physical identity to every electronic cent you move. Through the Bank Secrecy Act, these institutions are obligated to report “suspicious activity” and any transaction over a certain threshold directly to the government.

2. The Bitcoin Paradox: Transparency vs. Privacy

Bitcoin was originally championed as a way to bypass central authorities. However, the very technology that makes Bitcoin secure—the blockchain—is also its greatest liability for anyone seeking privacy.

Every single Bitcoin transaction is recorded on a public, permanent ledger. While your name isn’t written on the ledger, your “wallet address” is.

- The Trap: To buy Bitcoin, most people use exchanges (like Coinbase or Kraken). These exchanges are regulated just like banks and require full KYC documentation.

- The Link: The government uses sophisticated forensic software to track “hops” on the blockchain. Once they link a regulated exchange account to a specific wallet, the “pseudonymity” of Bitcoin evaporates. They can see every transaction that wallet has ever made or received, effectively defeating the original intent of a decentralized, private currency.

The Great Financial Compromise: Freedom or Duress?

This leads us to a much deeper, more philosophical question: Are we actually okay with these restrictions, or are they placed on us under duress?

Most of us check the “I Agree” box on a bank’s Terms and Conditions without a second thought. But is it truly a choice if the alternative is total exclusion from modern society? To live in the 21st century—to receive a paycheck, to pay a mortgage, or to buy a plane ticket—you must submit to the digital panopticon. When the only alternative to surveillance is financial exile, the “agreement” starts to feel a lot more like a mandate than a choice.

Should We Have the Right to Peer-to-Peer Privacy?

Should you be able to transfer your hard-earned money to anyone you want, whenever you want, without a third party “verifying” your identity?

- The Argument for Liberty: Proponents of financial privacy argue that money is a tool for autonomy. If the government can track every transaction, they have the power to freeze your life with a single keystroke. In this view, the ability to trade anonymously is a fundamental safeguard against overreach.

- The Argument for Security: The state argues that these restrictions are for our own good—to stop money laundering and tax evasion. They frame identity verification as the “price” we pay for a stable society.

The Last Bastion: The Paper Dollar

As digital systems become increasingly integrated with government surveillance and tax enforcement, the physical paper dollar stands as the last remaining method for “low-friction, low-identification” wealth transfer.

- No Ledger: When you hand someone a $20 bill, there is no digital record of the exchange.

- No Permission: You don’t need an app, an SSN, or a third-party intermediary to validate the trade.

- Immediate Finality: The transaction is finished the moment the paper changes hands.

The Bottom Line

Digital convenience comes at the cost of total visibility. While electronic transfers are fast, they are never truly private. For those who value the ability to move wealth without a permanent, government-accessible record, the “outdated” greenback remains the only technology that truly delivers on the promise of anonymity.

At CanIGetADollar.com, we recognize that in a world of digital tracking, the most powerful financial tool might just be the one in your physical wallet. Until a digital system exists that can truly replicate the “hand-to-hand” anonymity of a dollar bill, the physical remains the only place where true financial freedom lives.